27 March 2024

At Cantab Asset Management, we adopt a long-term approach to investing. What is meant by ‘buy and hold’ and why do we encourage our clients to think of themselves as ‘long-term investors’?

Our aim is to optimise performance over the medium to long term without exposing our clients to unnecessary risk. A prudent way of achieving this is to adopt a buy and hold investment strategy. Key research – mentioned below – supports the validity of this approach and highlights why we believe it is better for investors to be ‘tortoises’ and not ‘hares’.

Overview of the buy and hold philosophy

A buy and hold approach entails purchasing stocks and holding onto them for the medium to long term. Investors opt for this strategy with the aim of being rewarded for staying invested during the downs as well as ups of the market over time. Notable proponents of the approach include famed investment experts Peter Lynch and Warren Buffett.

Investors can find it challenging to stick to a buy and hold strategy as it may be tempting to change their investments, rather than to wait out difficult or volatile periods in the financial markets – but missing out on even a few of the best days in the market can be costly for returns. It should be noted, however, that holding onto a vastly underperforming stock can also be detrimental to performance. One way to help manage associated risks is to maintain a well-diversified portfolio. A buy and hold approach can be combined with active selection (for example, adjusting asset allocation) and can be employed as but one part of an investor’s broader financial plan.

In defence of being a tortoise: revealing research

Critics may assert that buy and hold investors can miss out on making trades at optimal times, unlike more speculative investors who try to ‘time the markets’ (effect trades at the ‘right time’ in an attempt to make a profit). However, timing the markets can be complex and difficult to achieve – even for experienced investors. As transactions are carried out on a much more regular basis with speculative investing than with a buy and hold approach, costs can soon add up. Rather than ‘timing the market’, a long-term investor allows ‘time in the market’ for assets to grow. We believe it is wisest to be a tortoise, not a hare, over the course of the investment journey. Indeed, recent research highlights key strengths of a buy and hold philosophy.

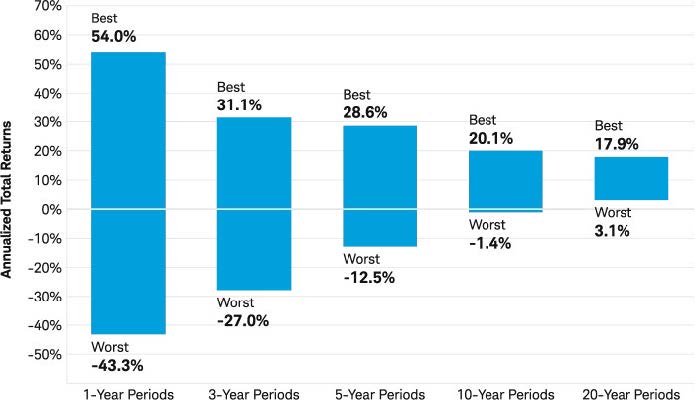

The below chart, produced by the Schwab Center for Financial Research, depicts the range (best and worst) of average annual returns of the S&P 500 Index from 1926 to 2019. The chart shows that the longer an investor’s time horizon, the less likely they are to experience a loss during that time (often referred to as lower ‘downside risk’). The chart also demonstrates some of the difficulties in attempting to predict short-term performance: for example, over a one-year period, the highest return was 54% and the lowest return was -43.3%; in contrast, over a 20-year period, the highest and lowest returns were both in positive territory.

Source: Schwab Center for Financial Research with data provided by Standard and Poor’s. Every 1-, 3-, 5-, 10-, and 20-year rolling calendar period for the S&P 500 Index was analysed from 1926 to 2019. The highest and lowest annual total returns for the specified rolling time periods were chosen to depict the volatility of the market. Returns include reinvestment of dividends. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is not indicative of future results.

Source: ARC / Suggestus, Celebrating 20 Years of Insight, published February 2024. The ARC Indices are constructed on the basis of around 350,000 underlying portfolios submitted by 125 private client and charity discretionary managers.

Additionally, ARC Research recently released data insights gained over the now 20-year timespan of the ARC Private Client Indices and the ARC Charity Indices. These indices provide objective performance data for both private client and charity investors, with the aim of helping them to contextualise their portfolio performance according to peer group.

ARC’s analysis of their two decades of gathered performance data reveals a pertinent and surprising point: while private client and charity portfolios have attempted to adapt their risk profiles in response to financial market conditions, this seems to have been to their disadvantage; the relative value of these portfolios has been eroded likely because they were acting on prevailing market sentiment. The research therefore supports a buy and hold investment approach, which discourages altering investments reactively.

Making hasty changes to investments in reaction to market fluctuations and changing sentiment can be reflective of cognitive or emotional bias. These terms refer to a systematic pattern of deviation from rational decision-making, often occurring subconsciously. Such biases can influence investment choices and potentially lead investors to make suboptimal financial decisions, which in turn may negatively impact their investment outcomes. Adopting a long-term perspective and avoiding ‘knee-jerk’ reactions may guard against the human tendency to act on cognitive and emotional biases.

Conclusion

A buy and hold strategy can reap rewards for investors over time. We recommend persevering for the long term (like the tortoise), rather than chasing quick gains and potentially stumbling (like the hare). Such an approach can allow investors to capitalise on opportunities that others might overlook – for example, focusing on attractively-valued companies with strong fundamentals and long-term growth potential. Although, as with any investment philosophy, there are criticisms against a buy and hold approach, our view is supported by research and long-term data, as outlined above. A buy and hold strategy to investing can be rewarding, provided investors monitor their investments appropriately, take professional advice where needed and, as the saying goes, ‘hasten slowly’.

There are risks inherent in all types of investment strategy. Moreover, what is appropriate for one investor may not be appropriate for another. It is vital to understand your personal financial goals and to consider investing as but one part of a greater whole. A qualified Financial Planner can help you to assess and plan your finances over different time horizons and to make tax-efficient financial decisions. We would be delighted to assist you in navigating the course of your financial journey.

Risk Warnings This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.