Introduction

Research shows there was a large increase in Google searches relating to annuities in 2022, potentially illustrating that retirees are more interested in purchasing these products following the sharp rise in interest rates. As annuity providers use bonds – primarily gilts – to underpin their annuity payments, we compare the potential returns of annuities and gilts and highlight some key points.

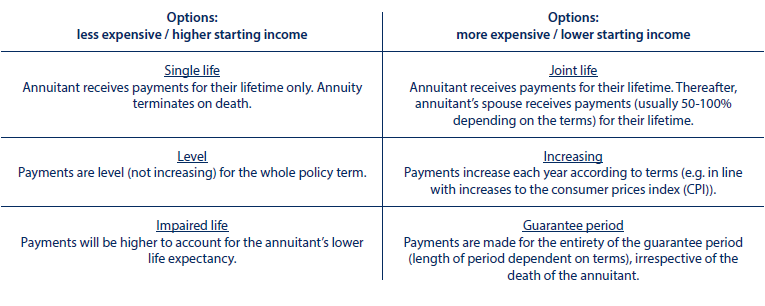

Overview of annuities

Annuities are contracts between annuity providers, usually large insurers, and annuitants, whereby the annuity provider commits to pay the annuitant a secure income for life in exchange for some or all of a pension fund (pension annuity) or a cash lump sum (purchased life annuity).

Annuity providers offer annuity rates based on annuitants’ personal circumstances – key factors are those that affect longevity, including age and health – and the options selected, such as level versus increasing payments. For example, one insurer quotes that being overweight can boost incomes by 10% to 15%, while those who have suffered from several heart attacks could receive an extra 30%. Interestingly, annuitants’ postcodes can affect their annuity rates, as postcodes associated with lower life expectancies can return more attractive rates than those with higher life expectancies. Some pensions (such as some older-style retirement annuity contracts) offer guaranteed annuity rates (GARs) which are often higher than annuity rates on the open market.

The table below shows some of the main features and how these can impact cost. Invariably, more expensive options result in lower income payments.

Income received from a pension annuity is classed as ‘earned income’ and subject to the PAYE tax system. Purchased life annuities follow a different taxation system where each income payment is deemed to include a return of capital plus interest. The capital repayment is tax free, while the interest payment is taxable as savings income.

Annuities and bonds

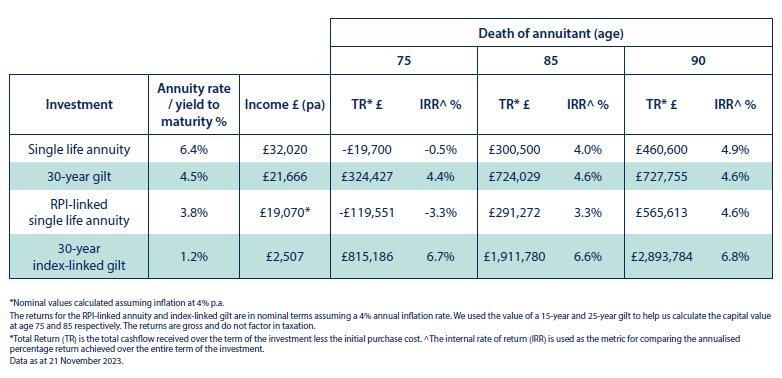

Seeking to match their potential liabilities, annuity providers invest into a portfolio of bonds, predominantly gilts. Providers stand to profit from the early deaths of annuitants, as their liabilities are extinguished or reduced and they can retain the invested capital, leading to headlines such as “Worsening life expectancy drives profit rise”. Would retirees be better off to invest in gilts themselves to fund their retirements?

We retrieved open market annuity quotes for our fictional retiree, ‘Harry’, who has a money purchase pension pot of £500,000. Harry is aged 60 and in good health with a life expectancy of 85. We compared the returns on the annuity to those potentially available on the 30-year conventional and index-linked gilts and calculated the monetary and annualised returns using some assumptions.

Certainty of income versus certainty of return

Annuities can be attractive because the amount of income is determined in advance (subject to changes in inflation for RPI-linked annuities). However, as the table illustrates, an annuity purchase may well be unattractive compared to a gilt (or other investment) portfolio where the capital is retained rather than given to the annuity provider. Results will vary and depend, inter alia, on how long the annuitant lives as well as investment returns.

The annuity returns are negative if Harry dies before age 76 as he receives less total income than the cost of the product. In contrast, Gilts are redeemed at par value at maturity, which gives certainty of the cashflows that will be received over the life of the Gilt. However, between the date of issuance and maturity, Gilts are traded on the market and prices will rise and fall based on various factors.

Clearly, annuities are more profitable the longer annuitants live beyond their expected date of death, whereas a conventional bond’s return is equal to its running yield if held to maturity.

Notably, the annuities pay out higher income than the gilts, as the annuity providers return some of the original capital to the annuitant. To mirror the annuity, Harry could sell some of his gilts each year to raise cash, or invest in a broader range of bonds, including corporate bonds or bond funds, to increase the yield. However, this will increase the credit risk.

Cantab recognises that forward thinking and thoughtful financial planning are key drivers of financial security and encourages the diversification of assets and wrappers to achieve this. Please contact your Cantab adviser for advice in your situation (advice@cantabam.com).

Risk Warnings This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.