It has been a rocky ride to kick off President Trump’s second term in office. The biggest surprise thus far is perhaps how surprised commentators and market participants have been by Trump doing exactly what he promised to do during his election campaign. Unlike during his first term – where there was much bluster and relatively little concrete action – this time around, there has already been significant policy implementation.

America First

Donald Trump ran on a policy platform committed to ‘America First’, focusing on economic growth driven by protectionism and deregulation; national security driven by strict immigration control and a robust military stance; and the promotion and restoration of ‘traditional’ American values. We have seen action already in each of these areas.

Tariffs

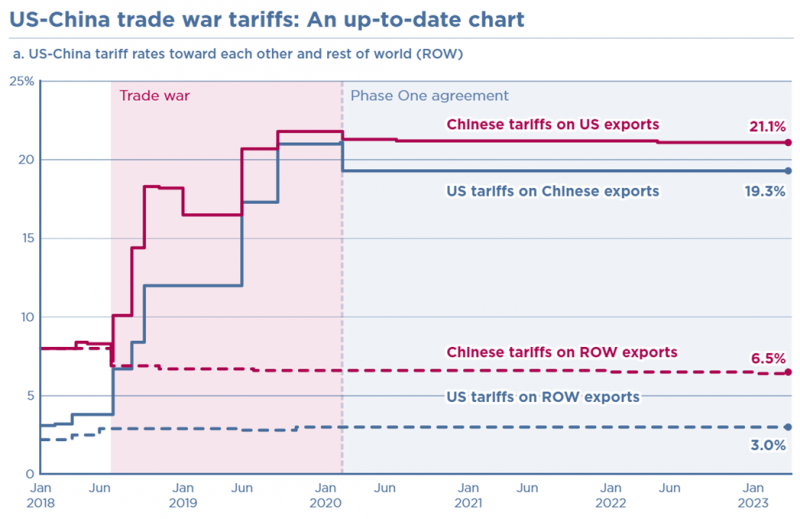

Trump believes that growth will be stimulated through protectionist trade policy. This message is consistent with his actions during his first term – the trade war with China was a significant economic feature of the 2018–2019 period. Between July 2018 and September 2019, the US imposed tariffs on over $300bn of trade, increasing the proportion of Chinese exports subject to US tariffs from close to zero to 66.4%. Retaliatory tariffs from China cover 58.3% of US exports, amounting to around $90bn. Whilst some relief was granted in a partial trade agreement in January 2020, the average tariff on exports between the two countries remains elevated at 19–21%.

It is challenging to assess the impact of tariffs in isolation. Economic theory tells us that barriers to trade (and, in particular, bilateral trade conflict) are damaging to manufacturers relying on overseas inputs and to consumers who suffer higher prices and reduced choice. Oxford Economics estimates that the US-China trade war cut US GDP by 0.2–0.4% and increased prices by 0.1–0.3%, whilst failing to shrink the US trade deficit in any meaningful way.

Since the start of February this year, tariffs have once again been front and centre of US economic policy. A first round of action focused on Fentanyl and immigration targeted Canada, China, and Mexico. This was swiftly followed by tariffs on global steel and aluminium, at a rate of 25%. The EU and Canada both retaliated with counter tariffs, raising fears of a protracted global trade war.

Source: Peterson Institute for International Economics.

There is undoubtedly a philosophical standpoint to support the idea that developed nations becoming excessively reliant on imports from countries with lower labour costs and standards is morally questionable. Becoming a nation unable to manufacture due to foreign competition has political and social ramifications that must be considered alongside the economic benefits of globalisation. However, a retaliatory trade war is a significant risk for the global economy and for the US manufacturing sector, which had been seeing early signs of recovery.

Foreign policy

During his campaign, Trump proposed significant investment in military capability whilst seeking to reduce US involvement in international conflicts and organisations such as NATO. He has repeatedly suggested that allied nations should be spending more on defence. He promised to confront Iran’s nuclear ambitions and to broker peace deals in the Middle East, as well as famously claiming that he would end the conflict between Russia and Ukraine ‘in 24 hours’.

Whilst some of Trump’s ideas have been unusual, he is correct in his assertion that much of the world has been a beneficiary of US investment in security over many decades. A realignment of responsibility in this regard does not seem unjust. Whilst 24 hours have been and gone in the President’s efforts to broker peace between Russia and Ukraine, it is fair to say that a deal looks closer now than at any time since the conflict began.

Peace and stability are clearly worthy goals in and of themselves. They are also essential for personal and business confidence to invest and grow. We are hopeful that developments will be positive for us all in both human and financial terms. In this area, perhaps more than any other, we should be reminded that Trump should be taken seriously despite his tendency for exaggeration and hyperbole.

Domestic and immigration policy

Immigration was a central focus of Trump’s campaign. He vowed to complete the US-Mexico border wall and deploy troops to combat drug cartels. His administration planned the largest deportation programme in US history, focusing on undocumented immigrants and the restriction of asylum claims. He also proposed ending birthright citizenship for children born in the US to non-citizen parents – a challenge to a fundamental constitutional right – and implementing a merit-based immigration system to prioritise skilled immigration.

Domestically, Trump has already targeted what he described as ‘woke’ ideologies, with a particular opposition to ‘gender indoctrination’ in schools. He has articulated a desire to repeal and replace the Affordable Care Act with a market-driven system, aiming at improved price transparency and lower prescription drug costs.

Many of these ideas have prompted concern from the liberal population but for the most part enjoy relatively wide popular support.

Market implications

The early response to Trump’s victory was positive for US markets, as participants anticipated a repeat of the positive impact seen during his first term. Recent weeks have seen markets correct, with a fair degree of catastrophising going on in the media. Whatever one’s personal view of Trump may be, we believe that his long-term impact on our clients’ ability to generate and grow wealth will be limited. Major policy is likely to be front-end loaded in his term, meaning we are likely to hear a lot of noise over the next couple of years.

We see risks to the US economy from higher-than-expected spending cuts driven by the Department of Government Efficiency (‘DOGE’). This could have significant effects on government, health, and education workers, which represent a significant portion of US payroll employees. The potentially inflationary impact of tariffs may make it more challenging for rates to fall in the US, which presents risks to both the housing sector and private credit and small businesses, who are disproportionately impacted by higher rates. We do not yet see these concerns fully priced in to markets, but the risks must be balanced with the potential positives of lower tax rates and an improved geopolitical environment.

Leah Bramwell

20 March 2025

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.