I wandered lonely as a cloud

Yes, the sun is shining, the daffodils are out, and the equity markets are… frosty?!

The past month has provided a good opportunity to test our mantra that what we are trying to achieve in our global equity fund is a philosophy and process that delivers superior risk-adjusted returns – by way of hunting for quality companies at attractive valuations – driven primarily by hanging in there on the way up and offering relative protection on the way down.

The chart below shows the performance of the Cantab global equity fund versus its IA Global peer group since the sector’s peak on January 23rd until March 6th, -2.3% versus -5.6%.

Cantab Global Equity fund performance vs IA Global sector

Source: FE Analytics; 23/01/2025 – 06/03/2025.

I am acutely aware that making any comment regarding such a short period of time amounts to a particularly narrow communication. Nevertheless, since we are all now living in interesting (crazy?) times, I thought it worthy of mention.

I also find the fund’s performance almost surprising. Alphabet, Amazon, TSMC and Microsoft have all suffered double-digit percentage declines, on a relative basis, over the past month. Moreover, some holdings saw double-digit-declines-in-a-day (PayPal, Akamai Technologies and Merck) during the reporting season.

I find it surprising because I am human and therefore, apparently, find losses twice as painful (and time consuming) as gains are joyful. And it serves as a reminder that the fund is, hopefully, balanced (something must have gone up), as I believe every long-term portfolio should be. If everything was going up at the same time, I would be worried, regardless of how nice it might feel.

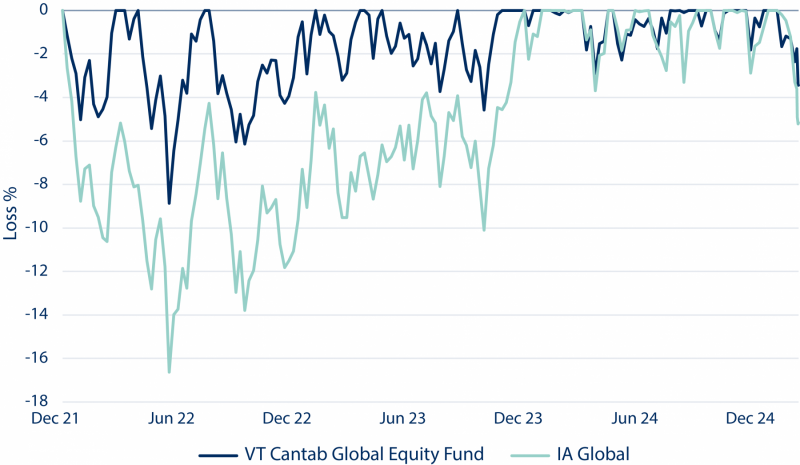

A chief concern of mine is that, at some point, the strategy’s characteristics will fail to protect to the downside. So far, however, so good. Be it the 2022 bear market, 2020’s COVID panic, 2015’s China slowdown, 2011’s Eurozone crisis, or the GFC, the strategy has delivered some level of protection. This cannot be a guarantee, however. For example, we do not screen for low-beta stocks, or volatility-scale our position sizes. But maybe there is something to be said for maintaining balance, while focusing on quality and relatively attractive valuations. While the strategy is not designed to shoot the lights out when making money is easy, nor is it specifically designed to be a safe harbour – this merely falls out of the bottom of the process, as if it was in its DNA.

Cantab Global Equity fund maximum drawdown vs IA Global sector

Source: FE Analytics; 31/12/2021 – 06/03/2025.

We tend not to get too much pushback in terms of this underlying philosophy. It appears to be a prudent strategy – and if it works for Warren Buffett & Co., what’s not to like?!

The devil, however, is in the detail. Often, I have been met with nodding heads when explaining philosophy and process. But when the conversation turns to recent trades – of which there are usually very few – there can sometimes be gasps of ‘why are you doing that?!’

In reality, buying quality companies at attractive valuations means buying quality companies at a point in time when other investors are having doubts as to whether they still are quality companies. How else do you engineer a margin of safety?

A few cherry-picked examples of stocks I have bought in the past: Estee Lauder in 2007 – ‘its brands are broken’ (plus ça change); Expedia in 2009 – ‘global recession, no-one’s travelling’; Microsoft in 2012 – ‘tech dinosaur’; Pearson in 2020 – ‘it’s Pearson’.

With the benefit of hindsight, most, if not all, successful investments seem obvious. At the point of initiation, however, there is almost always an element of discomfort (maybe there always should be an element of ‘lonely wandering’). The alternative is to buy the most popular names, but we all know where that can lead in the long run.

‘Time arbitrage’ is a great friend to the patient investor. All too often I have seen stocks go from hero to zero, when the truth is probably somewhere in between – is there an investor who hasn’t experienced the journey from excitement to despair? Discipline and patience, said Charlie Munger, are all you need.

Mark Wynne-Jones

Fund Manager

7 March 2025

Risk Warnings: This document is for institutional investors and financial advisors only. The views and opinions contained herein are those of Cantab Asset Management Ltd, are subject to change without notice, and should not be construed as investment advice or as an offer to invest. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. Investment parameters may change without notice. As with all equity-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. Investments in equities should therefore be viewed as a long-term investment. Past performance is not indicative of future performance.